Managing money is one of the most important life skills, yet many people struggle to build and maintain a realistic budget. Whether you are trying to save more, reduce debt, or simply understand where your money goes each month, effective budget management can help you create financial stability and long-term peace of mind.

A good budget is not about restricting every purchase or avoiding enjoyment. Instead, it gives you clarity, confidence, and control over your finances. When done correctly, budgeting helps you make smarter decisions, prepare for emergencies, and achieve your financial goals faster.

In this guide, you will learn what budget management is, why it matters, and how to build a practical budgeting system that works in real life.

What Is Budget Management?

Budget management is the process of planning, tracking, and controlling your income and expenses. It involves understanding how much money you earn, how much you spend, and how you can allocate your resources more effectively.

The main purpose of managing a budget is to ensure that your spending aligns with your financial priorities. This can include:

- Paying bills on time

- Saving for future goals

- Reducing unnecessary expenses

- Avoiding debt

- Building financial security

Budget management applies to individuals, families, businesses, and organizations. However, for personal finance, it mainly focuses on managing everyday expenses while preparing for future financial needs.

Why Budget Management Is Important

Many people believe budgeting is only necessary when money is tight. In reality, everyone benefits from having a financial plan, regardless of income level.

Here are some major benefits of effective budget management:

1. Better Financial Awareness

Budgeting helps you understand where your money is going. Many people underestimate small daily expenses, which can add up quickly over time.

Tracking your spending gives you a clear picture of your financial habits and helps identify areas where you can improve.

2. Reduced Financial Stress

Money problems are one of the leading causes of stress. A well-managed budget provides structure and predictability, reducing uncertainty about bills, savings, and expenses.

When you know your finances are under control, you feel more confident and less anxious.

3. Improved Savings

Without a budget, saving money often becomes an afterthought. Budget management allows you to prioritize savings and set aside funds consistently.

Even small contributions can grow significantly over time.

4. Debt Control

A budget helps prevent overspending and allows you to create a repayment plan for existing debts. By tracking your expenses, you can allocate more money toward loans, credit cards, or other financial obligations.

5. Goal Achievement

Whether you want to buy a house, travel, start a business, or retire comfortably, budgeting helps you plan for long-term financial goals.

Common Budgeting Mistakes

Before creating a budget, it is important to understand why many budgets fail.

Unrealistic Expectations

Some people create extremely strict budgets that eliminate all entertainment or personal spending. This approach is difficult to maintain and often leads to frustration.

A successful budget should be practical and flexible.

Ignoring Small Expenses

Daily coffee, food delivery, subscriptions, and impulse purchases may seem minor individually, but they can significantly impact your finances over time.

Not Tracking Spending

Creating a budget is only the first step. If you do not regularly monitor your spending, it becomes difficult to stay on track.

Forgetting Emergency Costs

Unexpected expenses such as medical bills, car repairs, or home maintenance can disrupt your finances if you are unprepared.

Giving Up Too Quickly

Budgeting is a skill that improves over time. Mistakes are normal, and adjustments are part of the process.

Steps to Create an Effective Budget

Building a budget does not have to be complicated. Follow these steps to create a system that works for your lifestyle.

Step 1: Calculate Your Total Income

Start by determining how much money you earn each month.

Include:

- Salary or wages

- Freelance income

- Business revenue

- Rental income

- Investment returns

- Side hustle earnings

Use your net income after taxes because this represents the amount you can actually spend or save.

Step 2: List All Expenses

Next, identify your monthly expenses. Divide them into two categories:

Fixed Expenses

These costs stay relatively consistent each month.

Examples include:

- Rent or mortgage

- Insurance

- Loan payments

- Internet bills

- Tuition fees

Variable Expenses

These change from month to month.

Examples include:

- Groceries

- Transportation

- Dining out

- Entertainment

- Shopping

Tracking both types of expenses helps you understand your spending patterns.

Step 3: Categorize Your Spending

Organizing expenses into categories makes it easier to identify areas for improvement.

Common budget categories include:

- Housing

- Utilities

- Transportation

- Food

- Healthcare

- Savings

- Debt repayment

- Entertainment

- Personal care

You can customize these categories based on your lifestyle and priorities.

Step 4: Set Financial Goals

Budgeting becomes more meaningful when connected to clear goals.

Short-term goals may include:

- Paying off a credit card

- Building an emergency fund

- Saving for a vacation

Long-term goals may include:

- Buying a home

- Investing for retirement

- Starting a business

Clear goals provide motivation and direction.

Step 5: Create Spending Limits

Once you know your income and expenses, assign spending limits to each category.

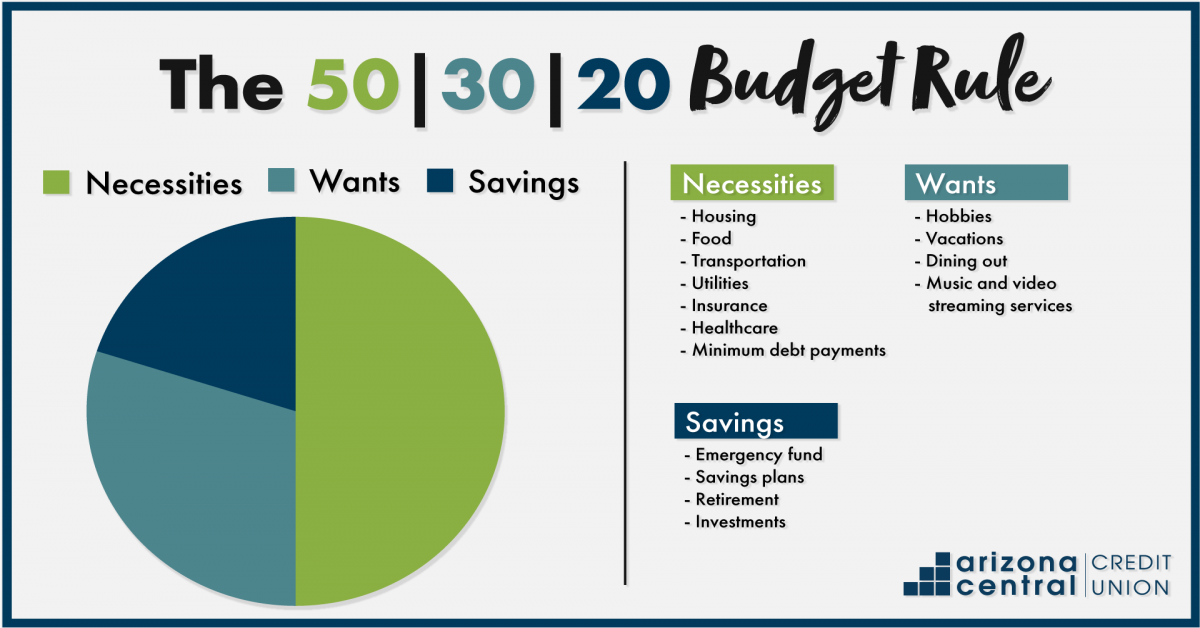

A popular approach is the 50/30/20 rule:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

While this framework is helpful, you can adjust percentages based on your financial situation.

Step 6: Track Your Progress

A budget only works if you monitor it consistently.

You can track expenses using:

- Budgeting apps

- Spreadsheets

- Banking tools

- Expense journals

Review your budget weekly or monthly to ensure you remain aligned with your goals.

Popular Budgeting Methods

Different budgeting methods work for different personalities and lifestyles.

Zero-Based Budgeting

In this method, every dollar has a purpose. Your income minus expenses should equal zero.

This approach encourages intentional spending and detailed financial planning.

Envelope Budgeting

This system uses cash envelopes for different spending categories.

Once an envelope is empty, you stop spending in that category until the next budgeting period.

Pay Yourself First

With this strategy, savings and investments are prioritized before other expenses.

Automatic transfers can help make this process easier.

Percentage-Based Budgeting

This approach allocates income percentages to categories such as savings, necessities, and entertainment.

It provides flexibility while maintaining financial balance.

How to Reduce Unnecessary Expenses

One of the main goals of budget management is identifying areas where money is being wasted.

Here are practical ways to cut unnecessary spending:

Cancel Unused Subscriptions

Many people pay for streaming services, memberships, or apps they rarely use.

Review subscriptions regularly and eliminate unnecessary costs.

Cook More Meals at Home

Frequent dining out can significantly increase monthly expenses. Preparing meals at home is often healthier and more affordable.

Avoid Impulse Purchases

Before making non-essential purchases, wait 24 hours. This simple habit can reduce unnecessary spending.

Compare Prices

Use discounts, coupons, and price comparison tools before buying products or services.

Reduce Energy Consumption

Lower utility bills by using energy-efficient appliances and reducing electricity waste.

The Importance of Emergency Funds

An emergency fund is a savings reserve used for unexpected expenses.

Without emergency savings, people often rely on credit cards or loans during financial crises.

Financial experts commonly recommend saving three to six months of living expenses.

Start small if necessary. Even a modest emergency fund can provide financial security and peace of mind.

Budget Management for Families

Family budgeting requires communication and cooperation.

Here are some tips for managing household finances effectively:

Set Shared Goals

Discuss financial priorities together, such as saving for education, vacations, or a new home.

Involve Everyone

Children can also learn valuable money management skills through budgeting discussions and responsibilities.

Plan for Irregular Expenses

Family expenses such as birthdays, school fees, and holidays should be included in the budget.

Use a Household Budget Calendar

Tracking bill due dates and upcoming expenses helps avoid missed payments.

Budget Management for Students

Students often face financial challenges due to limited income and educational expenses.

Here are useful budgeting tips for students:

- Track daily spending

- Avoid unnecessary debt

- Buy used textbooks

- Use student discounts

- Create a meal plan

- Limit entertainment expenses

Learning financial discipline early can create long-term financial success.

Digital Tools for Budget Management

Technology has made budgeting more convenient than ever.

Popular budgeting tools can help users:

- Monitor expenses automatically

- Set savings goals

- Receive spending alerts

- Analyze financial habits

- Track investments

Digital budgeting tools simplify money management and improve financial awareness.

How Inflation Affects Budgeting

Inflation increases the cost of goods and services over time. As prices rise, budgeting becomes even more important.

To manage inflation effectively:

- Review your budget regularly

- Adjust spending priorities

- Focus on essential expenses

- Increase savings when possible

- Look for additional income opportunities

Adapting your budget to changing economic conditions helps maintain financial stability.

Building Long-Term Financial Habits

Successful budget management is not about temporary restrictions. It is about building sustainable financial habits.

Healthy financial habits include:

- Saving consistently

- Spending intentionally

- Avoiding unnecessary debt

- Reviewing finances regularly

- Investing for the future

Small daily decisions can create major financial improvements over time.

The Psychological Side of Budgeting

Money management is not only about numbers. Emotions and behavior also play a major role.

Common emotional spending triggers include:

- Stress

- Boredom

- Social pressure

- Impulse buying

Understanding your spending habits can help you make more mindful financial decisions.

Developing discipline and self-awareness is essential for long-term success.

Tips for Staying Consistent With Your Budget

Consistency is often the biggest challenge in budgeting.

Here are practical ways to stay motivated:

Automate Savings

Automatic transfers reduce the temptation to spend money intended for savings.

Review Goals Frequently

Regular reminders of your financial goals help maintain focus and motivation.

Allow Flexible Spending

Including some entertainment or personal spending makes budgeting more sustainable.

Celebrate Progress

Recognize financial milestones such as paying off debt or reaching savings targets.

Adjust When Necessary

Life changes, and your budget should evolve with your circumstances.

Signs Your Budget Is Working

A successful budget often leads to noticeable improvements in financial well-being.

Positive signs include:

- Reduced financial stress

- Increased savings

- Fewer late payments

- Better debt management

- Greater confidence with money

- Improved financial decision-making

Budgeting may take time to master, but the long-term benefits are substantial.

Final Thoughts

Budget management is one of the most powerful tools for achieving financial stability and long-term success. It allows you to take control of your money, reduce stress, and work toward meaningful financial goals.

The key to successful budgeting is consistency rather than perfection. Start by understanding your income and expenses, create realistic spending plans, and make adjustments as needed. Over time, even small financial improvements can lead to significant results.

Whether you are managing personal finances, supporting a family, or preparing for future goals, a well-structured budget provides the foundation for smarter financial decisions and greater financial freedom.

By developing healthy money habits today, you can build a more secure and confident financial future for yourself and your family.