Managing money is one of the most important life skills, yet many people learn it through trial and error. Whether you earn a modest salary or a high income, financial success often depends less on how much you make and more on how well you manage what you have. Good money habits can reduce stress, improve financial security, and help you achieve long-term goals like buying a home, traveling, starting a business, or retiring comfortably.

The good news is that money management does not have to be complicated. Small, consistent changes can create a major impact over time. In this guide, you will learn practical money management tips that can help you build a stronger financial future without feeling overwhelmed.

Why Money Management Matters

Poor financial habits can lead to debt, anxiety, and constant financial pressure. On the other hand, effective money management gives you more freedom and control over your life. When you know where your money is going, you can make better decisions and avoid unnecessary financial mistakes.

Money management is not just about saving. It includes budgeting, spending wisely, investing, reducing debt, planning for emergencies, and building healthy financial habits.

1. Create a Monthly Budget

A budget is the foundation of good financial management. It helps you understand your income, expenses, and spending patterns. Without a budget, it is easy to overspend without realizing it.

Start by listing all your sources of income. Then write down your monthly expenses, including rent, groceries, transportation, utilities, subscriptions, and entertainment. Divide your expenses into two categories:

- Fixed expenses

- Variable expenses

Once you see the full picture, you can identify areas where you may be spending too much.

A popular budgeting strategy is the 50/30/20 rule:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

This method keeps your finances balanced while allowing room for enjoyment and future planning.

2. Track Your Spending Habits

Many people underestimate how much they spend on small daily purchases. Coffee runs, online shopping, food delivery, and impulse purchases may seem harmless individually, but they add up quickly.

Tracking your spending helps you stay aware of where your money goes. You can use a budgeting app, spreadsheet, or even a notebook. The goal is consistency.

After tracking your expenses for a month, review your spending patterns. You may notice habits that are quietly draining your finances. Awareness is often the first step toward better financial decisions.

3. Build an Emergency Fund

Unexpected expenses are part of life. Medical bills, car repairs, job loss, or home maintenance can happen at any time. Without savings, these situations often lead to debt.

An emergency fund acts as a financial safety net. Ideally, you should aim to save three to six months’ worth of living expenses. However, if that feels overwhelming, start small.

Even saving a small amount every month can help you build financial stability over time. Keep your emergency fund in a separate savings account so you are less tempted to spend it.

4. Avoid Unnecessary Debt

Debt can become a major obstacle to financial freedom. While some forms of debt, like mortgages or student loans, may be necessary, high-interest debt such as credit card balances can quickly spiral out of control.

Before making a purchase, ask yourself:

- Do I really need this?

- Can I afford it without borrowing?

- Will this purchase improve my life long term?

If you already have debt, focus on creating a repayment plan. Two common methods include:

The Snowball Method

Pay off smaller debts first to build momentum and motivation.

The Avalanche Method

Pay off debts with the highest interest rates first to save more money over time.

Whichever method you choose, consistency is key.

5. Save Before You Spend

One of the best financial habits is paying yourself first. Instead of saving whatever is left at the end of the month, move a portion of your income into savings as soon as you get paid.

Automating your savings can make this process easier. Set up automatic transfers to your savings account every payday. This removes temptation and helps you stay disciplined.

Even small contributions matter. Saving regularly is more important than saving large amounts occasionally.

6. Set Clear Financial Goals

Financial goals give your money purpose. Without goals, it is easy to spend impulsively and lose direction.

Your goals may include:

- Buying a house

- Starting a business

- Paying off debt

- Traveling

- Building retirement savings

- Creating multiple income streams

Divide your goals into:

- Short-term goals

- Medium-term goals

- Long-term goals

Make your goals specific and realistic. For example, instead of saying “I want to save money,” say “I want to save $5,000 in the next 12 months.”

Having clear targets keeps you motivated and focused.

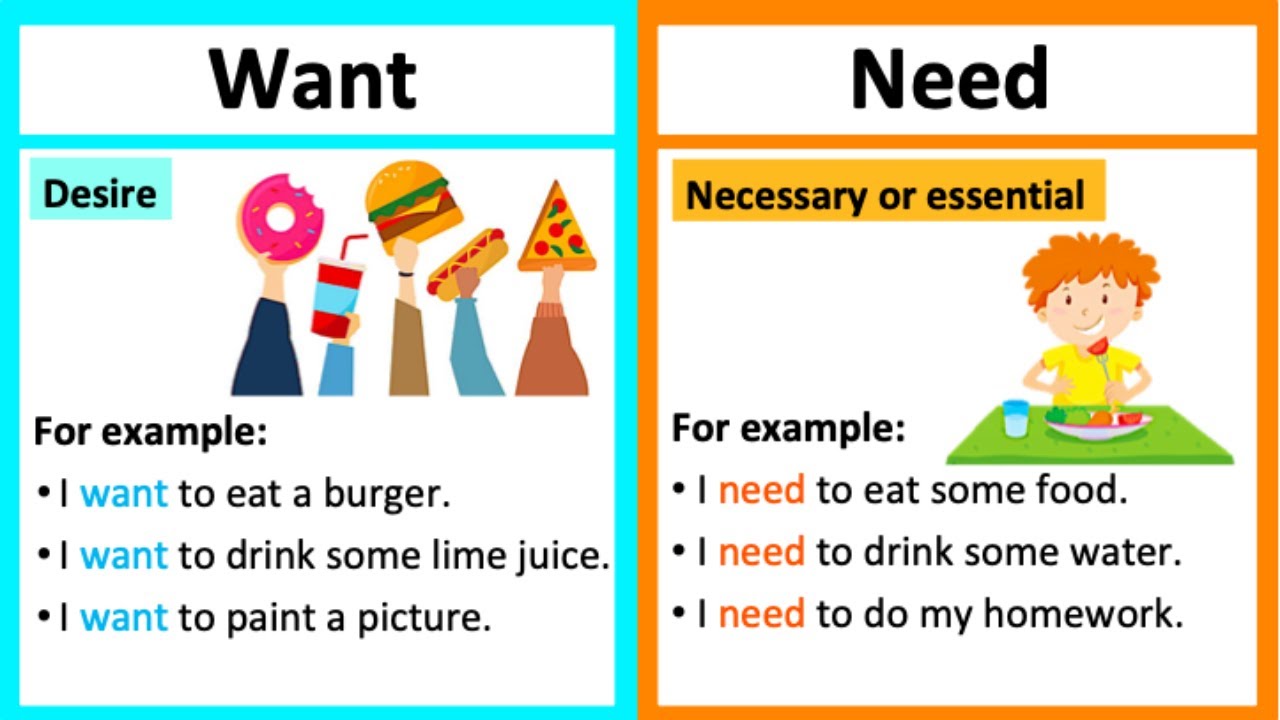

7. Learn the Difference Between Needs and Wants

One of the biggest challenges in money management is distinguishing between essential expenses and lifestyle desires.

Needs include:

- Housing

- Food

- Utilities

- Healthcare

- Transportation

Wants include:

- Luxury items

- Expensive gadgets

- Dining out frequently

- Premium subscriptions

This does not mean you should never spend on enjoyment. The key is balance. Spending intentionally helps you avoid financial regret later.

Before making non-essential purchases, consider waiting 24 hours. This simple habit can reduce impulse spending significantly.

8. Invest for the Future

Saving money is important, but investing helps your money grow over time. Inflation reduces purchasing power, which means money sitting in a basic savings account may lose value over the years.

Investing allows you to build wealth through:

- Stocks

- Mutual funds

- Real estate

- Retirement accounts

- Exchange-traded funds (ETFs)

If you are new to investing, start by learning the basics. You do not need to become a financial expert overnight. Even small investments made consistently can grow substantially through compound interest.

The earlier you start investing, the more time your money has to grow.

9. Live Below Your Means

Many financial problems occur because people try to maintain lifestyles they cannot truly afford. Social media often creates pressure to spend on luxury experiences, trendy products, or status symbols.

Living below your means does not mean living poorly. It means spending less than you earn and avoiding unnecessary financial pressure.

Simple ways to live below your means include:

- Cooking at home more often

- Buying quality items instead of trendy ones

- Avoiding lifestyle inflation

- Comparing prices before purchases

- Limiting unnecessary subscriptions

Financial peace often comes from simplicity rather than constant consumption.

10. Increase Your Financial Knowledge

Financial education is one of the best investments you can make. The more you understand money, the better decisions you can make about saving, spending, investing, and planning for the future.

Read books, listen to podcasts, follow credible financial experts, and stay informed about personal finance topics.

Key areas to learn about include:

- Budgeting

- Credit scores

- Taxes

- Investing

- Retirement planning

- Insurance

- Passive income

You do not need a finance degree to manage money well. Continuous learning can improve your financial confidence and decision-making.

11. Review Your Financial Situation Regularly

Money management is not something you set up once and forget. Your financial situation changes over time, so regular reviews are important.

At least once a month:

- Check your budget

- Review your savings progress

- Monitor debt repayment

- Evaluate your spending habits

- Adjust financial goals if needed

Regular financial check-ins help you stay on track and catch problems early.

12. Protect Your Financial Health

Managing money is not only about growing wealth. It is also about protecting what you already have.

Important steps include:

- Having health insurance

- Protecting personal information

- Monitoring credit reports

- Using strong passwords for banking apps

- Avoiding financial scams

Financial security requires both smart planning and careful protection.

13. Develop Multiple Sources of Income

Relying on one source of income can be risky. If that income disappears unexpectedly, your financial stability may suffer.

Many people improve their finances by creating additional income streams such as:

- Freelancing

- Online businesses

- Investing

- Selling digital products

- Rental income

- Side hustles

Even a small extra income can help you pay off debt faster, increase savings, or invest more consistently.

14. Practice Delayed Gratification

Modern culture encourages instant spending and quick rewards. However, strong money management often requires patience.

Delayed gratification means resisting short-term temptations for larger long-term benefits. For example:

- Saving for a purchase instead of using credit

- Investing instead of impulse shopping

- Paying off debt before upgrading your lifestyle

This mindset can dramatically improve your financial future over time.

15. Teach Good Money Habits to Your Family

Financial habits are often learned at home. Teaching children and family members about budgeting, saving, and responsible spending can create long-term benefits for future generations.

Simple lessons such as saving part of an allowance, comparing prices, or setting savings goals can build financial awareness early in life.

Open conversations about money also reduce financial stress within families.

Common Money Management Mistakes to Avoid

Even financially responsible people can make mistakes. Here are some common errors to watch out for:

Ignoring Small Expenses

Tiny daily purchases can quietly damage your budget over time.

Not Saving for Emergencies

Unexpected situations become far more stressful without savings.

Relying Too Much on Credit Cards

High-interest debt can quickly grow if balances are not paid off.

Failing to Plan for Retirement

Waiting too long to invest can reduce long-term wealth potential.

Emotional Spending

Shopping to relieve stress or boredom often leads to regret later.

Recognizing these mistakes early can help you stay financially healthy.

Final Thoughts

Good money management is not about perfection. It is about building consistent habits that support your financial goals and overall well-being. Small improvements made regularly can lead to major financial progress over time.

Start with the basics:

- Create a budget

- Track your expenses

- Build savings

- Reduce debt

- Invest for the future

The most important step is taking action. You do not need to change everything overnight. Focus on gradual progress and stay committed to improving your financial habits.

With patience, discipline, and smart planning, you can build a more secure and financially confident future.